Columns

Cartoons

Podcasts

Tipsheet

Videos

MY ACCOUNT

Account Settings

Newsletter Subscriptions

Log Out

Subscribe

LOGIN

Login

MY ACCOUNT

Account Settings

Newsletter Subscriptions

Comment Settings

Log Out

LOGIN

Subscribe

Tipsheet

Columns

Cartoons

Podcasts

Videos

Contact Us

Terms & Conditions

Privacy Policy

California - Do Not Sell My Personal Information

California CCPA Notice

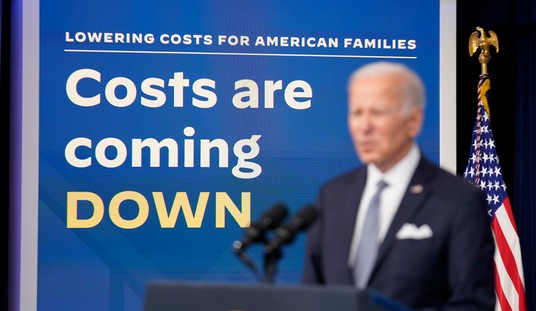

Oh Look, Another Terrible Inflation Report

Spencer Brown

Here’s Why One University Postponed a Pro-Hamas Protest

Madeline Leesman

There's a Big Change in How Biden Now Walks to and From Marine One

Leah Barkoukis

Leader of Columbia's Pro-Hamas Encampment: Israel Supporters 'Don't Deserve to Live'

Guy Benson

The Gaza Genocide Narrative Suffers Another Major Deathblow

Matt Vespa

Trump Responds to Bill Barr's Endorsement in Typical Fashion

Leah Barkoukis

US Ambassador to the UN Calls Russia's Latest Veto 'Baffling'

Leah Barkoukis

Advertisement

Columns

Iran's Nightmares

Victor Davis Hanson

Amanpour Repeats CNN's Gaza Lie

Brad Slager

Restore Order and Crush the Campus Jihadist Thugs

Josh Hammer

Leftist Reporters Pretend They're Not Partisan News Squashers

Tim Graham

The Problem Is Academia

Laura Hollis

Washington Should Clip Qatar’s Media Wing

Natalie Ecanow

The Most Disturbing Part of It

Erick Erickson

Inept Microsoft is Compromising National Security

Julio Rivera

Leftist Activists Said 'Believe All Women' Didn’t Apply to Me

Paula Scanlan

Biden Fails Moral Leadership Test in Handling Anti-Semitic Campus Protests

Jenny Beth Martin

Sanctuary Cities Defund the Police to Pay for Illegal Immigration

William Davis

All Columns

View Cartoon

Liberal Reporter Sees Some Serious Media Frustration on This Issue

Matt Vespa

About Those Alleged Posts of Snipers on the Campuses of Indiana and Ohio State Universities

Matt Vespa

Polling on Support for Mass Deportations Has Some Surprising Findings. But Does It Matter?

Leah Barkoukis

Advertisement

Trending

1

The Gaza Genocide Narrative Suffers Another Major Deathblow

Matt Vespa

2

There's a Big Change in How Biden Now Walks to and From Marine One

Leah Barkoukis

3

Iran's Nightmares

Victor Davis Hanson

4

Liberal Reporter Sees Some Serious Media Frustration on This Issue

Matt Vespa

5

Oh Look, Another Terrible Inflation Report

Spencer Brown

6

Leader of Columbia's Pro-Hamas Encampment: Israel Supporters 'Don't Deserve to Live'

Guy Benson

7

About Those Alleged Posts of Snipers on the Campuses of Indiana and Ohio State Universities

Matt Vespa

8

Will Jewish Voters Stop Voting for the Democrats Who Want to Kill Them?

Kurt Schlichter

9

How Many More Times Will Joe Biden Mention This at the Podium This Year?

Matt Vespa

10

Here’s Why One University Postponed a Pro-Hamas Protest

Madeline Leesman

Advertisement

Members Only

Polling on Support for Mass Deportations Has Some Surprising Findings. But Does It Matter?

Leah Barkoukis

Trump Has More Enthusiasm From Voters Than Biden Ever Will

Sarah Arnold

Amanpour Repeats CNN's Gaza Lie

Brad Slager

DeSantis Reveals How Florida Colleges Will Respond to Pro-Hamas Students

Madeline Leesman

Wow: Biden Just Endorsed a Disastrous, Unpopular Economic Policy That Will Inflict Even More Harm

Guy Benson

Another Poll on Battleground States Is Here to Toss Cold Water on Biden's Supposed Gains

Rebecca Downs

Advertisement

How Many More Times Will Joe Biden Mention This at the Podium This Year?

Matt Vespa

Thousand of Illegal Immigrants With Pounds of Fentanyl Apprehended by Border Patrol

Sarah Arnold

NYC Construction Workers: 'F*ck Joe Biden,' We Want Trump

Sarah Arnold

Pro-Hamas Students Set Up Another Camp... but This Jewish Student Isn't Cowering

Spencer Brown

Trump Speaks Out About 'Monumental' SCOTUS Immunity Arguments

Sarah Arnold

DHS Has a Warning for Foreign Students Participating in Anti-Israel Protests

Sarah Arnold

Trending on Townhall Media

There Was a Coup Attempt Against Karine Jean-Pierre, and the Details Are Something

Maybe the Supreme Court Should ‘Take a Walk:’ A Deep Dive Into Thursday’s Oral Arguments

Avoid UCLA-Educated Doctors--Seriously

Forget the Matchup Polls. This Number Is What Should Terrify Team Biden.

No One Shocked by Newsom's Amendment Proposal Going Down in Flames

Justice Alito Mocks Judge Pan's 'SEAL Team Six' Hypothetical in Trump Immunity Arguments

Biden Campaign's Warning to Media About WH Correspondents' Dinner Should Be in a Trump Ad

Biden's Latest Regulations Will Crash the Electric Grid

Katie Pavlich

USC Cancels Commencement Ceremony Amid Pro-Hamas Antics by Lunatic Students

Matt Vespa

Trump Has More Enthusiasm From Voters Than Biden Ever Will

Sarah Arnold

AOC Doubles Down on Support for Pro-Hamas Protests

Rebecca Downs

The Biden White House Is Still at Odds With The New York Times

Rebecca Downs

Advertisement

A Principal Was Removed, Faced Threats for Making Racist Comments. There's Just One, Major Problem.

Mia Cathell

Wow: Biden Just Endorsed a Disastrous, Unpopular Economic Policy That Will Inflict Even More Harm

Guy Benson

Is It Wrong to Deny Someone a Job Because They Have Demonic Face and Neck Tattoos?

Townhall Video

Newsom Unveils Bill in Response to Arizona's Impending Pro-Life Law

Madeline Leesman

NYPD Patrol Chief Shuts AOC Down After She Posts Defense of Pro-Hamas Agitators at Columbia

Katie Pavlich

Advertisement

NY Times Journalist Tries Defending Pro-Hamas Students. It Doesn't End Well for Her.

Townhall Video

Iran-Backed Terrorists Resume Attacks on U.S. Service Members in the Middle East

Spencer Brown

Another Poll on Battleground States Is Here to Toss Cold Water on Biden's Supposed Gains

Rebecca Downs

White House Attempt to Cover for Biden's Latest Gaffe Might Be Its Most Brazen Yet

Spencer Brown

US, 17 Other Nations Issue Joint Statement Calling on Hamas to Release Hostages

Leah Barkoukis

Advertisement

Stocks Tank After Disastrous First Quarter GDP Report

Spencer Brown

Could Texas Ban ‘Gender Nonconforming’ Teachers From Schools?

Madeline Leesman

Should Republicans Be Concerned About the Pennsylvania Primary Results?

Guy Benson

Terrorists Launch Attacks on Americans Building Biden’s Gaza Pier

Katie Pavlich

Florida Has Carried Out an Impressive Evacuation Operation in Haiti

Leah Barkoukis

Advertisement

Mike Davis' Internet Accountability Project Calls on Senate Republicans to Break Up Big Tech

Rebecca Downs

Police at UT Austin Had the Perfect Response to a Pro-Hamas Activist Flipping Them Off

Matt Vespa

The Pro-Hamas Activist Who Accosted Alec Baldwin Went Totally Insane During Piers Morgan Interview

Matt Vespa

Biden Administration's New Overtime Rule Blasted as an 'Attack on Small Businesses'

Leah Barkoukis

Secret Service Agent Assigned to Kamala Harris Suffers What Looks Like a Mental Breakdown

Matt Vespa

Advertisement

Students at Another Ivy League University Get Ready to Set Up Encampment

Leah Barkoukis

Here's the Video Exposing What NYU's Pro-Hamas Students Really Think

Matt Vespa

NYT Claims Trump Is Getting 'Favorable Treatment' from the NYPD

Sarah Arnold

NYPD Arrests Dozens Who Besieged Area Near Chuck Schumer's Home

Matt Vespa

Texas Doesn't Take Passive Approach to Anti-Israel Mobs

Sarah Arnold

Advertisement

Columbia Prof Who Called to Defund the Police, Now Wants Police to Protect Him from Anti-Israel Protests

Sarah Arnold

Mike Johnson Addresses Anti-Israel Hate As Hundreds Harass the School’s Jewish Community

Sarah Arnold

White House Insists Biden Has Been 'Very Clear' About His Position on Pro-Hamas Campus Chaos

Spencer Brown